OUR INVESTMENT CASE

Accelerating growth and driving shareholder value

At Inchcape, we leverage our global automotive Distribution expertise, strong OEM partnerships, and data-driven capabilities to deliver sustainable growth and shareholder value. With a focus on operational excellence and expanding in high-growth markets, we are uniquely positioned to capitalise on the evolving mobility landscape.

Inchcape is a FTSE 250 company listed on the London Stock Exchange and the world’s leading independent automotive Distributor. The business is capital-light, highly cash generative and has delivered consistently high return on capital employed. This financial profile, driven by a Distribution-led model, positions Inchcape as a compelling long-term investment. Inchcape has been listed on the London Stock Exchange since 1958, with a long-term track record of delivering value for shareholders.

Medium term targets: 2025 – 2030, through-the-cycle

Our transformation

Since 2016, Inchcape has transformed into a Distribution-led business, managing the end-to-end automotive value chain on behalf of OEM partners. Where we operate retail sites, these form part of our Distribution offering – allowing us to get closer to our markets, better understand customers' needs, and generate the insights that make us a market-leading Distributor.

We have exited retail-only operations across a number of markets, including the sale of UK retail operations in 2024, tripled our OEM partnerships, more than doubled new vehicle volumes and pursued value-accretive M&A, including the 2022 acquisition of Derco.

Learn more about our Distribution model and our Accelerate+ strategy.

2025 highlights

60 +

OEM brand partners

vs. 20 in 2016

40 +

Distribution markets

vs. 23 in 2016

£ 9.1 bn

Annualised distribution revenue

vs. £3.4bn in 2016

Three pillars of our investment case

The leading global automotive Distributor

- Long-term, diversified OEM portfolio

- Deep competitive moat through technology

- Scaled and diversified geographic footprint

With an attractive financial profile

- Growth driven by market outperformance

- Resilient operating margins

- Highly cash generative and capital efficient

Driving shareholder value

- Clear dividend policy

- Commitment to on-going share buybacks

- Value-accretive acquisitions

"Inchcape is the leading independent global provider of an essential part of the value chain in the global automotive industry – Distribution. Our business model drives our strong financial profile – which is capital-light, with resilient margins and healthy free cash flow generation, helping us to deliver high returns."

Chief Financial Officer

PILLAR 1

Leading global automotive distributor

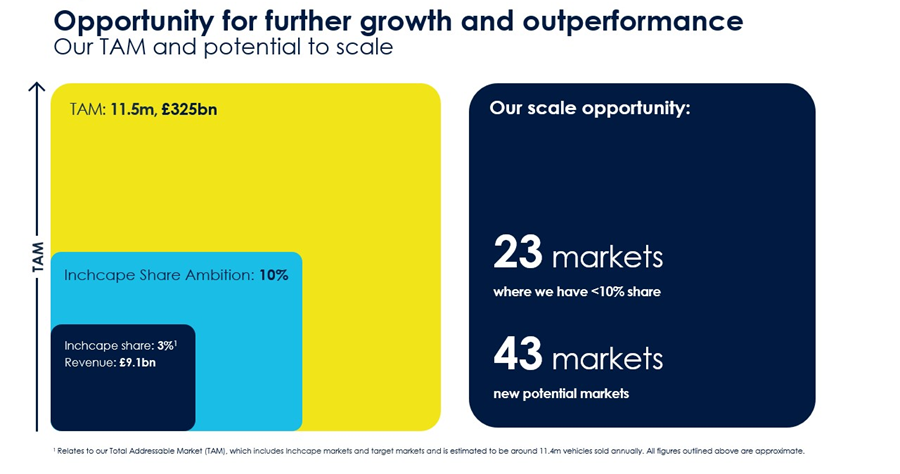

Our opportunity for growth

Inchcape's Total Addressable Market (TAM) covers small to mid-sized markets which are more complex, have high GDP growth, with low motorisation rates, estimated at around 10.8 million vehicles sold annually. Inchcape currently holds a 3% share of this TAM, underlining the scale of the opportunity ahead. The long-term ambition is to reach a 10% market share in each of our markets.

Discover our global markets.

Explore our regions

PILLAR 2

Attractive financial profile

Growth driven by outperformance

Our diverse global presence helps us navigate market volatility. While overall market growth is expected at 1–2% annually, we aim to outperform by growing market share through our existing contracts and new wins, driving 2–3% volume growth. Together this means targeting 3–5% organic compound growth before acquisitions.

2 -3 %

Market outperformance

Resilient operating margins

Around 85% of our revenue comes from vehicles and 15% from parts. We generate gross margins of 15–18%, with higher margins on parts (40–45%) than vehicles (10–15%). Our variable cost base supports resilient operating margins, with a typical automotive distributor in the range of 5-7%, and with our business at a historic blended margin of c.6%.

6 %

operating margins

Highly cash generative

Inchcape's capital-light Distribution model consistently delivers strong free cash flow, with a track record of converting approximately 100% of profit after tax (PAT) to free cash flow. Optimising working capital, especially in newly acquired businesses, has been a key driver and by managing the end-to-end automotive value chain on behalf of OEM partners – rather than operating exclusively as a retailer – Inchcape maintains a lower capital base. We expect to generate an aggregate of £2.5 billion in free cash flow through to the end of 2030, from the start of 2025.

100 %FCF

PAT conversion

Capital efficient and high ROCE

Return on Capital Employed (ROCE) reflects our continued focus on high-margin, cash generative and capital-light Distribution. The exit of retail-only operations and the integration of value-accretive acquisitions has supported efficient use of capital. As we scale our Distribution platform through technology, contract wins, and bolt-on M&A, we expect ROCE to remain consistently high between 25–30%.

25 -30 %

ROCE

PILLAR 3

Driving shareholder value

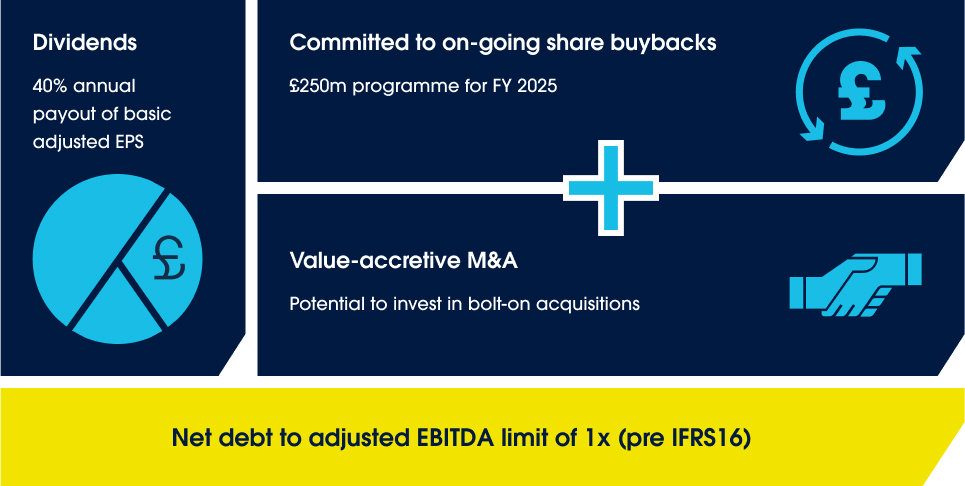

Our capital allocation policy

We have set ambitious targets to grow our business responsibly, seeking to create significant value for all our stakeholders. Inchcape’s capital allocation policy balances three priorities: a progressive dividend targeting an annual payout of 40% of basic adjusted earnings per share (EPS); an on-going commitment to share buybacks; and value-accretive M&A to grow the Distribution platform. The Group manages this within a self-mandated net debt to adjusted EBITDA limit of 1x (pre-IFRS16).

Investor contact

Discover more

Results, Reports & Presentations

Discover moreDiscover our latest results, reports, and presentations in one place, helping investors stay informed and aligned with our long-term strategy.

Discover more

Sustainability for investors

Learn moreExplore how our Sustainability practices are embedded into our strategy, operations, and long-term growth plans, driving sustainable value for investors.

Learn more