What support do consumers need to accelerate the transition to New Energy Vehicles?

The automotive industry is undergoing an unprecedented transformation, driven by rapid technological advancement, evolving regulatory landscapes and global action to address climate change.

Understanding consumer sentiment around New Energy Vehicles (NEVs), alongside broader vehicle ownership trends, helps us tailor our strategies to support an accelerated transition to lower-carbon mobility. The transition to NEVs is well underway globally, but in recent years we have seen varying sentiment towards NEVs and differing pace of adoption across countries.

To explore how consumers feel about NEVs, unpack their motivations and ambitions for vehicle ownership, and investigate barriers to ownership, we recently surveyed more than 6,000 consumers across 13 countries in Latin America and Asia-Pacific. Shared in our Drivers of Change report, our findings indicate that despite overall positive consumer sentiment, there are still barriers to adoption, and the automotive industry and Governments need to continue to work together to develop technology, bring down costs and build the infrastructure necessary to encourage a faster transition.

Positive momentum, but barriers to adoption remain

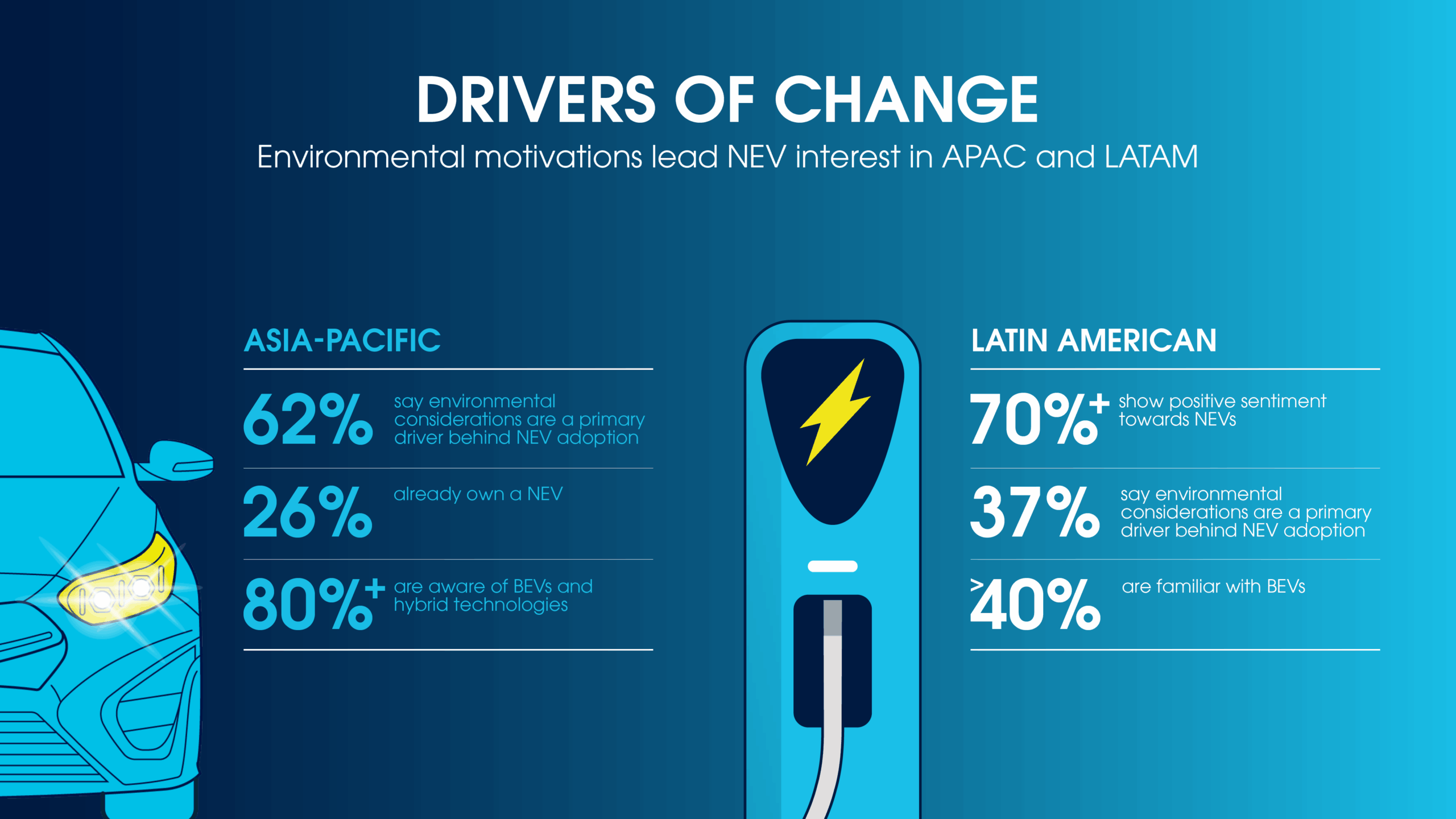

Encouragingly, we see that intent to purchase NEVs is growing. For example, 53% of respondents in Ecuador and 49% of respondents in Colombia and Peru are considering purchasing a BEV in the next two years. Consumers in Asia Pacific are overwhelmingly positive about NEVs and 57% see themselves owning a NEV. Having a more positive impact on the planet is driving this trend, with 62% in APAC and 37% in Latin America citing environmental considerations as a key driver.

What’s holding consumers back?

Although there’s a positive consensus around NEVs in markets across APAC and Latin America, market maturity is a critical factor as intent to buy varies. In Latin America, respondents identified infrastructure as the main barrier, fewer than half of respondents in the countries we surveyed agreed that charging availability is adequate. In both regions, affordability was the single greatest obstacle identified by respondents, with 68% in APAC and 24% in Latin America viewing NEVs as still too expensive. Although these barriers are common across multiple regions, they are especially pronounced in some of the countries we operate in with lower economic development and limited fiscal incentives.

Policy incentives and consumer education are key to moving forward

In Latin America, tax reductions on vehicle purchase was the most widely supported policy measure, supported by 45–58% of respondents across countries. Reduced circulation permit fees, which include lower parking fees for low emissions vehicles, were favoured by up to 61% of consumers, especially in Colombia and Costa Rica. Subsidies for home charger installation and battery recycling and replacement programmes are also a priority.

In Asia-Pacific, approximately 58% of respondents call for better consumer education, such as information on battery lifespan and charging, reaching a high of 65% in the Philippines. Moreover, nearly two-thirds of Singaporeans agree that governments should set deadlines to phase out ICE vehicles, signaling support for national policy transitions.

Our findings confirm the NEV transition is unfolding at different speeds in different markets worldwide. A single, uniform approach will not succeed. Instead, the path forward must be responsive to each country’s unique infrastructure, socio-economic conditions, and market maturity. And distributors have a role to play by raising awareness, educating stakeholders, tailoring the right mix of vehicles in product portfolios and stimulating demand.

With the right collective approach – informed by local-market insights – we can accelerate the mobility transition to lower carbon transport solutions.

Liz Brown Chief Strategy & Sustainability Officer